Landlord tax relief changes explained

What are the changes? FIND OUT more on changes to landlord tax relief

Landlord tax relief in action VIEW IT tax relief in action

Other taxes for residential landlords DISCOVER other taxes for residential landlords

Landlord tax relief changes explained

What are the changes?

FIND OUT more on changes to landlord tax relief

Landlord tax relief in action

VIEW IT tax relief in action

Other taxes for residential landlords

DISCOVER other taxes for residential landlords

This article details a set of changes to landlord tax relief that took place from 2016 to 2021.

As all of these changes are now effective, the information here is historical. However, if you’re looking for a way to save money on your taxes, read our article about allowable expenses for landlords.

From April 2017, landlords saw the money they could write off for tax purposes drop by 25% year on year until April 2021. And while the UK Government has claimed that 82% of landlords won’t be impacted, our research showed that over 40% of landlords† believe they will have to pay additional tax as a result of the changes to the rules around landlord tax relief.

So, to help you better understand how the Government’s plans could impact your wallet, we’re examining what the changes to landlord tax relief entail and what they could mean for you. That way when it comes to balancing your landlord books, you’ll be well-versed in what to expect and (hopefully) won’t be blindsided with any surprise costs.

What are the changes to landlord tax relief?

Landlords could previously deduct finance costs, like mortgage interest, from their earnings to reduce the income tax they needed to pay. However, in 6 April 2017, the Government changed income tax relief for residential landlords by replacing the existing system with a basic tax reduction of 20% on whichever of the following is the smallest:

- Finance costs: total interest on mortgage, loans or overdraft.

- Property profits: net rental income.

- Adjusted total income: earnings after deducting losses, tax relief and personal allowance.

As a result, tax relief is given as a reduction in tax liability instead of a reduction to taxable income, meaning landlords will have to declare all of their rental income, pay income tax on the full amount, and then claim back 20% of this as credit, or 45% for those who receive the highest rate.

The government hopes that these changes to landlord tax relief will help prevent the highest earning landlords from receiving the biggest income tax relief, but they won’t affect registered companies or landlords of furnished holiday homes.

Why are changes to landlord tax relief being brought in incrementally?

Rather than introducing reforms to landlord tax relief in one fell swoop, the Government chose to phase the changes in gradually between April 2017 and April 2021. This means that, for a time, both the old and new methods for calculating income tax relief will apply to varying degrees.

The split between the existing method of personal finance deduction and the new 20% basic rate reduction will be worked out as follows:

| Year | Existing method | New method |

|---|---|---|

| 2016-17 | 100% | 0% |

| 2017-18 | 75% | 25% |

| 2018-19 | 50% | 50% |

| 2019-20 |

25%

|

75%

|

| 2020-21 | 0% | 100% |

So, in 2019-20 tax year, landlords can deduct 25% of their mortgage interest under the old system and 75% will qualify for the 20% tax credit under the new system (down from 50% for the 2018-19 tax year).

When you’re creating your landlord checklist for each new tax year, it could be a good idea to make sure you’re fully up to speed with how to accurately record what tax you should be paying as a landlord because any minor slipups could result in pricey fines from HMRC.

Landlord tax relief in action

So that you’re well aware of what these changes mean for you, we’ve decided to examine how three example landlords* throughout the UK with varying incomes could be affected by the incremental changes to landlord tax relief.

* These examples are fictional and are not based on any individual persons. The amounts cited are for illustrative purposes only, using fictional numbers. The calculations have been made following the Government’s example, which can be found here. All calculations are based on current tax rates and allowances.

Find out how the changes could affect Martin

'The Part Timer'

2 x properties owned

FIND OUT HOW the changes could affect Martin, the part timer

Find out how the changes could affect Michael

'The Professional'

6 x properties owned

FIND OUT HOW the changes ould affect Michael, the professional

Find out how the changes could affect Martin

'The Part Timer'

2 x properties owned

FIND OUT HOW the changes could affect Martin, the part timer

Find out how the changes could affect Michael

'The Professional'

6 x properties owned

FIND OUT HOW the changes ould affect Michael, the professional

Meet Martin 'The Part Timer'

| Location: | Ipswich |

|---|---|

| Income: | Works full time, earning £34,000 per year |

| Landlord experience: | Three years |

| Properties: | Two |

“

I bought additional properties specifically to let them out to tenants. I’m planning for my future, and buy-to-let is my nest egg for retirement. I’ve read a bit about these changes and I’m worried I’m going to be worse off.

”

If renting out residential properties is a significant side-line that supplements your main income, you could be hit by the upcoming changes to buy-to-let tax relief.

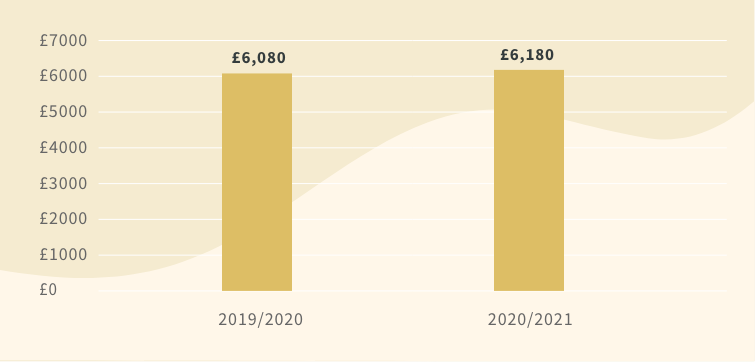

The cost for Martin

Let’s assume Martin earns a pre-tax salary of £34,000 from a full-time job, plus £11,500 per year from his two properties, and pays £3,600 mortgage interest annually. Here’s how the amount of tax Martin pays could be affected over the course of the next two years.

Below are the figures displayed in the graph above:

- 2019/2020: £6080

- 2020/2021: £6180

You can see how these calculations were made and learn how to work out your expected income tax for yourself using the UK Government’s explainer guide.

How Martin is impacted

Martin will be largely unaffected by the changes to landlord tax relief until the final year of the transition. That’s because until then, he’s allowed to deduct enough of his personal finance costs to keep him under the higher rate income tax threshold.

Because the changes could push Martin’s taxable income up it could also:

- Push him into a higher income tax bracket.

- Make him eligible for the high income child benefit charge.

If you’re in Martin’s position and you want more information on the background to these changes, click here.

Meet Martin

'The Part Timer'

| Location: | Ipswich |

|---|---|

| Landlord experience: | Three years |

| Income: | Works full time, earning £34,000 per year |

| Properties: | Two |

“I bought additional properties specifically to let them out to tenants. I’m planning for my future, and buy-to-let is my nest egg for retirement. I’ve read a bit about these changes and I’m worried I’m going to be worse off.”

If renting out residential properties is a significant side-line that supplements your main income, you could be hit by the upcoming changes to buy-to-let tax relief.

The cost for Martin

Let’s assume Martin earns a pre-tax salary of £34,000 from a full-time job, plus £11,500 per year from his two properties, and pays £3,600 mortgage interest annually. Here’s how the amount of tax Martin pays could be affected over the course of the next two years.

| Year | Tax |

|---|---|

| 2019-20 | £4,320 |

| 2019-21 | £4,320 |

You can see how these calculations were made and learn how to work out your expected income tax for yourself using the UK Government’s explainer guide.

How Martin is impacted

Martin will be largely unaffected by the changes to landlord tax relief until the final year of the transition. That’s because until then, he’s allowed to deduct enough of his personal finance costs to keep him under the higher rate income tax threshold.

Because the changes could push Martin’s taxable income up it could also:

- Push him into a higher income tax bracket.

- Make him eligible for the high income child benefit charge.

If you’re in Martin’s position and you want more information on the background to these changes, click here.

Meet Michael 'The Professional'

| Location: | Bristol |

|---|---|

| Income: | Full-time landlord, earning £110,000 per year |

| Landlord experience: | Ten years |

| Properties: | Six |

“

I was lucky enough to inherit a portfolio of properties recently, which means I don’t need to have another job. I’m worried about how the changes are going to affect my sole source of income and my ability to continue paying the leftover mortgages.

”

If, like Michael, renting out residential properties is your main source of income, the buy-to-let tax changes that will be phased in until April 2020 could have a big impact on your bottom line.

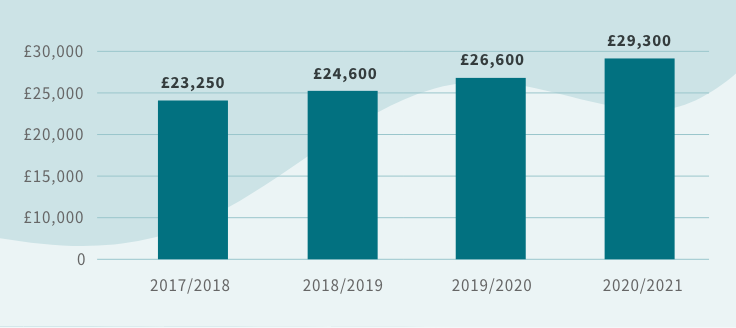

The cost for Michael

Let’s assume Michael earns £110,000 per year from rental income and pays £27,000 mortgage interest annually. Here’s how the amount of tax Michael pays could be affected the money landlords can write off for tax purposes drops by 25% each year between 2017 and 2020.

Below are the figures displayed in the graph above:

- 2017/2018: £23,250

- 2018/2019: £24,600

- 2019/2020: £26,600

- 2020/2021: £29,300

You can see how these calculations were made and learn how to work out your expected income tax for yourself using the UK Government’s explainer guide.

How Michael is impacted

Because of the large number of properties Michael owns and the income he receives as a result, the changes could push Michael’s taxable income up considerably.

This means that, for landlords like Michael, managing finances and other allowable expenses will become an even more important part of your rental experience.

Meet Michael

'The Professional'

| Location: | Bristol |

|---|---|

| Landlord experience: | Ten years |

| Income: | Full-time landlord, earning £110,000 per year |

| Properties: | Six |

“I was lucky enough to inherit a portfolio of properties recently, which means I don’t need to have another job. I’m worried about how the changes are going to affect my sole source of income and my ability to continue paying the leftover mortgages.”

If, like Michael, renting out residential properties is your main source of income, the buy-to-let tax changes that will be phased in until April 2020 could have a big impact on your bottom line.

The cost for Michael

Let’s assume Michael earns £110,000 per year from rental income and pays £27,000 mortgage interest annually. Here’s how the amount of tax Michael pays could be affected the money landlords can write off for tax purposes drops by 25% each year between 2017 and 2020.

| Year | Tax |

|---|---|

| 2019-20 | £4,320 |

| 2020-21 | £4,320 |

You can see how these calculations were made and learn how to work out your expected income tax for yourself using the UK Government’s explainer guide.

How Michael is impacted

Because of the large number of properties Michael owns and the income he receives as a result, the changes could push Michael’s taxable income up considerably.

This means that, for landlords like Michael, managing finances and other allowable expenses will become an even more important part of your rental experience.

Other taxes that affect residential landlords

From adhering to the latest legislation to keeping on top of repairs, life as a landlord is jampacked with responsibility, which is why we’ve created our complete guide to being a landlord to help make renting out your property that bit more straightforward.

One of your most important tasks of being a landlord is ensuring you’ve calculated your income and taxes accurately to stay on the good side of the taxman. But this change to landlord tax relief discussed isn’t the only thing that dictates the total amount you owe HMRC each year. Here’s some other taxes to be aware of to help your landlord numbers add up as they should.

Stamp Duty Land Tax

Stamp Duty Land Tax (or SDLT) is a tax payable on properties over £125,000 in England, Wales and Northern Ireland. For second properties, a flat rate of 3% is now added to the basic stamp duty, regardless of the purchase price.

From 1 March 2019, the period allowed in England and Northern Ireland for filing a Stamp Duty Land Tax return and paying the tax reduces from 30 days to 14 days. Failure to comply with the 14-day deadline could lead to interest and penalties. In both Scotland and Wales, the deadline for filing returns and paying tax will remain at 30 days.

Wear-and-tear allowance

The 10% Wear and Tear Allowance was removed in April 2016 and now landlords can only claim for actual costs incurred. Wear and tear is now treated like other allowable expenses, with itemised receipts needed as evidence to support any claims made in your tax return – which makes keeping receipts and records all the more important.

But defining wear and tear versus damage caused by a tenant can be tricky, which is why it’s a smart idea to create a detailed inventory list to help prevent any potential disputes between landlord and tenant. Any inventory list worth its salt should detail the condition of all the furniture, fittings and fixtures in your home as well as the state of the paintwork, walls and flooring.

Why not take some photos of your rental property before tenants move in so you have proof of its condition prior to their living in it? And to ensure that both you and your tenants are fully aware of the condition of your buy-to-let, consider carrying out a walkthrough inspection at the beginning of a tenancy agreement and both signing an inventory list to confirm that both parties agree with it.

How to keep on top of your landlord accounts

As well as keeping tabs on your rental income, it’s important that you try to keep records and paperwork for all the expenses you encounter as a landlord – especially as the amount of tax you’ll pay depends on how much you’ve spent maintaining your property.

Remember to list your allowable expenses too because these can be deducted from your earnings and lower the amount that you’ll be taxed on. Allowable expenses include landlord insurance, contents insurance, maintenance and repair fees.

By remaining organised and getting to grips with how landlord tax legislation affects you, the likelier you are to avoid getting things wrong and facing costly fines from HMRC. Remember, if you’re unsure of any aspect of your obligations or how to complete them, it’s sensible to seek advice from a qualified professional.

Life as a landlord can be challenging. Protecting your property isn’t.

From keeping tenants happy to balancing your accounts, life as a landlord can be tricky. With AXA landlord insurance, we make protecting property simple. Meaning you get the protection that’s right for you when you need it most.

† Based on AXA research of 382 UK landlords conducted in March 2017

The examples in this article are fictional. The amounts cited are for illustrative purposes only, using fictional numbers. Calculations are not based on any individual persons.

†† Analysis of changes for landlords taken from UK Government information available at: https://www.gov.uk/government/publications/restricting-finance-cost-relief-for-individual-landlords/restricting-finance-cost-relief-for-individual-landlords