How to calculate your rental yield

AXA’s guide how to calculate return on investment as well as everything else you need to know about rental yield.

If you’re thinking about becoming a landlord, or you want to add another property to your portfolio, it’s important to understand rental yield. You’ll need to recognise what a good rental yield is and be able to calculate it. Having a sound understanding will help you make better investment decisions and ensure your buy-to-let mortgage is affordable.

AXA’s guide will explain what rental yield is and how to calculate it with a quick and easy step-by-step guide. We’ll also help you understand why rental yield matters for investments and what’s considered a ‘good’ rental yield.

What is rental yield?

Rental yield is the potential returns on property investment through rent. It’s a percentage figure that’s calculated using the annual rental income and the value of the property.

Landlords and investors use rental yield to monitor the value of their property investments and portfolios. Things like a fluctuating housing market, property prices, interest rates and demand growth can all affect rental yield.

Why does rental yield matter for investments?

When it comes to investing in property, achieving a good rental return is really important. Before you purchase a buy-to-let property, you’ll need to work out what to charge for rent to make your investment worthwhile. If your income falls short of your expenditure, or you’re just breaking even, something as simple as an unexpected boiler repair or a leaky roof can leave you seriously in the red.

With that being said, rental yield isn’t the only thing you need to consider when it comes to property investments. You’ll also need to look at things like capital growth and tenant demand before purchasing a buy-to-let. For example, you could buy a property with a very good rental yield, but if the area shows no sign of house price growth or you struggle to find suitable tenants, the investment may not seem as attractive.

What’s the difference between gross and net rental yield?

It’s important to understand the difference between gross and net rental yield because it determines what type of calculation you need to do. There’s an easy way to understand the difference between the two:

![]()

Gross rental yield is everything before expenses.

Gross rental yield is calculated using the price of the property and the income generated by the property.

![]()

Net rental yield is everything after expenses.

Net rental yield is calculated using the price of the property, the income generated by the property and the associated costs and fees of owning a property.

Calculating the gross rental yield for a single property is easier than you might think. We’ve put together this quick step-by-step guide to help you.

To calculate your gross rental yield, just follow these three steps:

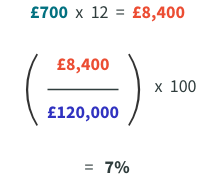

| 1. | Multiply your monthly rental income by 12 to get your annual rental income. |

| 2. | Divide that figure by the property’s purchase price |

| 3. | Multiply that figure by 100 to get your gross rental yield percentage |

Example of a gross rental yield calculation

Amber purchased a property for £120,000 and collects £700 every month from her tenant. What would Amber’s gross rental yield be?

Here’s how the calculation looks for Amber:

If you haven’t purchased the property yet, just use the current market value and your anticipated rental income. And, if your rent is paid weekly, just multiply the figure by 52 to get your annual rental income.

Who would use the gross rental yield?

A gross yield percentage is used when the specific costs of owning a property aren’t known. That’s why gross rental yield is often used by mortgage lenders when considering the affordability of buy-to-let mortgages, and by estate agents and local studies of average rental yields for the same reason.

Equally, the gross rental yield can be used as a metric to quickly compare different investments which is useful when you’re looking at multiple properties.

But while gross rental yield is a great way to see a quick snapshot of what your investment returns could be, it doesn’t consider the associated costs and fees that come with owning a property. That’s why we turn to the net rental yield calculation.

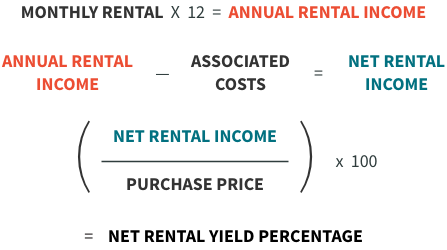

The net rental yield can offer a more comprehensive understanding of investment returns because it also considers the expense of owning a property.

It’s calculated by taking the annual rental income minus the costs associated with owning a buy-to-let property, then dividing by the property’s purchase price or the current market value. Here’s a step-by-step guide on how to calculate net rental yield.

| 1. | Multiply the monthly rental income by 12. |

| 2. | Subtract the annual costs of owning a property (Mortgage payments, insurances, general maintenance). |

| 3. | Divide that by the property’s purchase price or current market value. |

| 4. | Multiply that figure by 100 to get the percentage. |

Here’s what the calculation looks like:

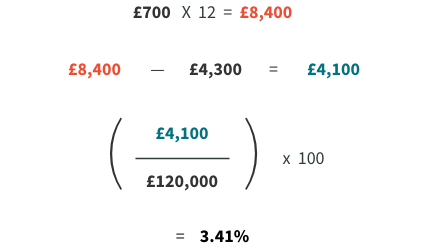

Example of a net rental yield calculation

Amber bought her property for £120,000 and collects £700 every month from her tenant. She has a £100,000 buy-to-let mortgage at a fixed interest rate of 3%. With an interest-only mortgage, her repayments are £250 per month, or £3,000 per year. She typically spends £1,300 every year on general maintenance, repairs and property and landlord insurances, giving her annual costs of £4,300.

Here’s how the calculation looks for Amber:

What is a good rental yield?

There isn’t a one-size-fits-all approach when it comes to defining a ‘good’ rental yield. The ideal percentage will change depending on the location and whether it’s a residential property or student accommodation. As a general rule, a gross rental yield between 5 and 6 percent would be considered ‘good’ and anything above 7 percent would be ‘very good’.

Above all, a good net rental yield should cover all the necessary property expenses while allowing landlords to make a reasonable return on investment.

When you’re looking to invest in a new property, it can be tempting to look in an area with big demand for rentals or where capital growth is high. Equally, you might want to buy a property that’s below the market value. But if the amount you collect in rent doesn’t cover your mortgage payments and other the other costs associated with owning a property, you’ll likely have a poor rental yield and disappointing return on investment.

How to maximise your rental yield

With a fluctuating property market and changing mortgage interest rates, a property’s rental yield varies depending on outside factors. However, there are a few things you can do to maximise your rental yield.

1) Adjust the rent

If your rent is lower than the market rate, you might able to increase it depending on your tenancy agreement. Equally, if your rent is too high compared to the property or the area, you might want to consider reducing it so you don’t miss out on income if your property is without tenants for periods of time.

2) Consider a house in multiple occupation (HMO)

HMOs are owned by private landlords and rented by three or more people. There are a number of practicalities to consider before converting your property to an HMO, but it could lead to a more profitable investment because you can collect rent from more tenants.

3) Assess your outgoings

It can be easy to overlook your regular property outgoings but there are simple things you can change that would lead to big savings. Whether it’s re-mortgaging to find a better deal, or sourcing cheaper trades people to carry out maintenance and repairs, it’ll go a long way in maximising your net rental yield.

What is capital growth and how is it calculated?

Capital growth is the term used to describe the increase in the value of a property over a period of time. It’s sometimes called capital appreciation.

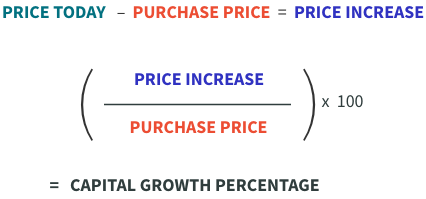

Capital growth is calculated by comparing the current market value of a property to the amount paid when it was bought originally. The percentage increase represents the return on investment from a capital growth point of view.

Here’s what the calculation looks like:

Property prices do tend to increase over time. However, in the short to mid-term, they’re known to fluctuate and can actually decrease. That’s why it’s difficult to predict what a property’s price will be in the future and capital growth can only be accurately defined at the time of calculation.

When it comes to selling a buy-to-let property, you might need to pay capital gains tax on any profit you make. How much tax you’ll pay will vary depending on your personal circumstances and how much profit you make.

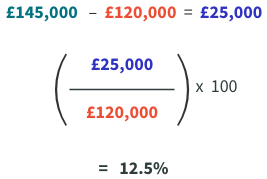

Example of a capital growth calculation

If we take Amber’s property and imagine it increases in value from £120,000 to £145,000 price in five years’ time, the following calculation would be used to show the property’s capital growth.

Here’s how the calculation looks for Amber:

Property prices do tend to increase over time. However, in the short to mid-term, they’re known to fluctuate and can actually decrease. That’s why it’s difficult to predict what a property’s price will be in the future and capital growth can only be accurately defined at the time of calculation.

When it comes to selling a buy-to-let property, you might need to pay capital gains tax on any profit you make. How much tax you’ll pay will vary depending on your personal circumstances and how much profit you make.

AXA landlord insurance from £173*

Insure your rental property with AXA today and join the two thirds of UK landlords who have the right cover in place1. With one less thing to worry about, you focus on what really matter to you.

* 10% of our customers paid this or less between January and March 2026.

1 According to GlobalData 2016 Report.