Selling your second property?

If you have recently acquired a second property –whether that’s through a purchase, inheritance or another method – you may be thinking of selling it rather than trying to manage two properties.

If you live far away from the second property and aren’t regularly using it as a holiday home, then ensuring its upkeep and maintenance can be quite difficult. Additionally, managing the ongoing costs of council tax, mortgages and more for two properties at the same time can be financially prohibitive.

For these reasons and more, you may be considering selling your second property…but what if there was another way? For those who have two properties, renting out one of them can be a great way to generate some additional income without giving up a place that may have sentimental value or which could have a better financial value in the future.

When does renting it out make sense?

If the market is expected to keep growing

According to HomeLet, in 2021 rent is the highest it has ever been in the UK. Meanwhile the Guardian reports that are rising at their fastest rate in over 15 years and Savills predicts that property values will continue to rise well into 2025. Renting a property out, even if just for a few years, could help you wait until your second property hits peak pricing so that you sell it at its highest value.

You have a ‘rentable’ property

Is the property near a city full of young professionals or in the catchment for a great school system? That can mean a constant stream of tenants available to rent out your property. If you’re less sure of being able to consistently fill the property, then it may not be worth renting it out.

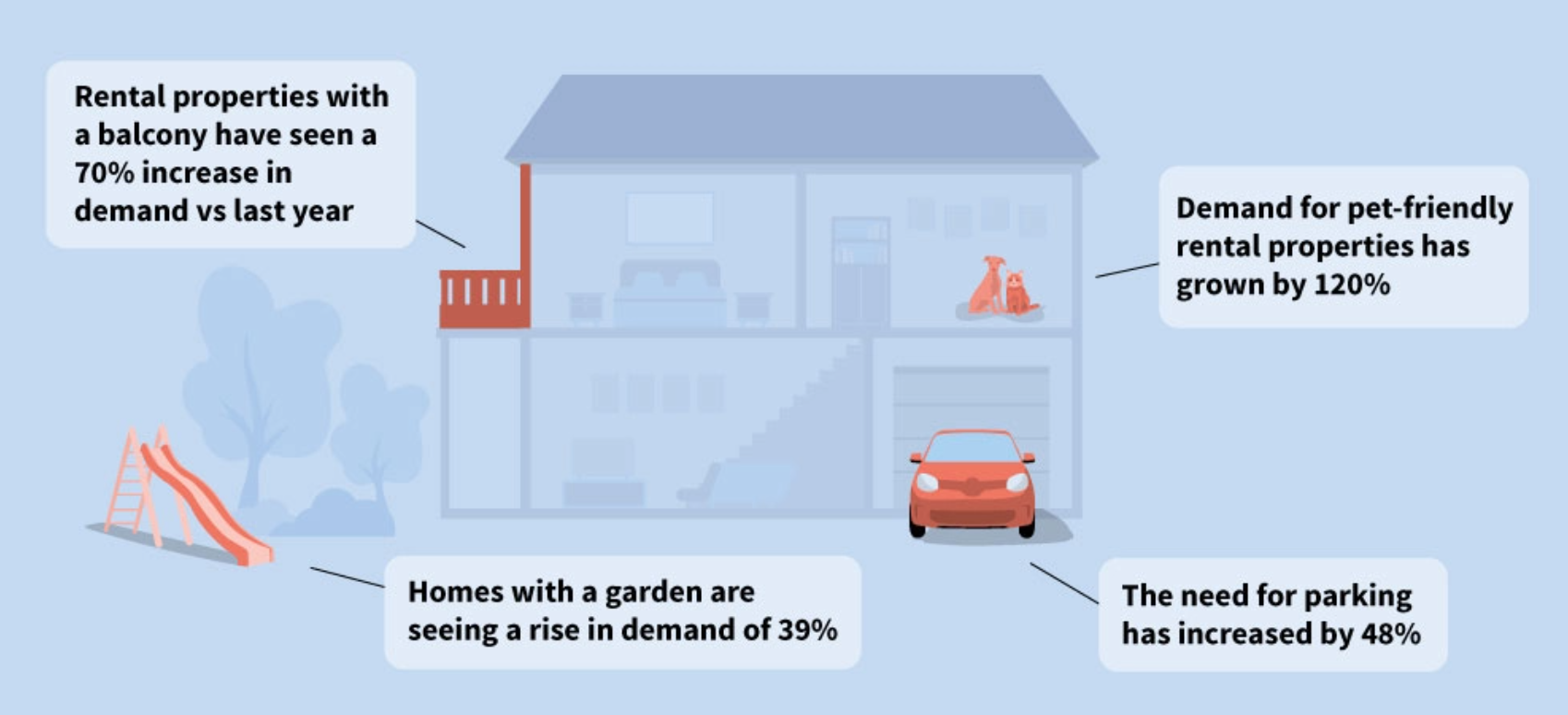

While the location and price have always been big considerations for potential tenants, the Buy Association says that the following things have grown in importance for tenants over the last year:

If you need more time

You may need more time for any number of reasons, but renting can help you hold on to a property until the right moment. This might be giving you time to figure out minimising the amount of taxes you’ll pay on the sale of a second property, it might be a way to generate income needed to get the house into a sellable state, or it might give you time to decide if your move to another location is really what you want long term.

It is financially viable for you

If you need the money generated from the sale of this property in order to afford your next property, then renting won’t give you a quick influx of money. However, if this property is struggling to sell, it can be much faster to get a renter in place than it is to get a buyer. If you don’t need the equity that’s tied up in your second property, then renting could at least cover the mortgage and, if possible, help generate some extra income.

If you’re sure the rent you charge would cover the costs of keeping the property, then renting may make sense for you. If you’re not quite sure how to judge your potential rental income, then take a look at our guide on calculating your rental yield.

You can attract good tenants

You’ll want to make sure you can find the right kind of tenants. Maybe you’re close to a university campus and are nervous about the toll that student life could have on your property. Of course students aren’t a deal-breaker, just make sure that you’re carrying out thorough tenant reference checks to reduce risk and help you find the right tenants for your property.

Real advice from AXA customer & landlord, Andreea Plant:

References are crucial. Speak to their current landlord to get a reference from them and possibly a previous landlord too if you can. If in doubt I’ll ask for a second reference, even a character reference. And then I always ask for credit checks on all tenants and make it quite clear to them that it’s something that’s mandatory for a tenancy.

Read more advice from AndreeaPros & Cons to holding onto your second home

Pros

- Gives the property value time to appreciate

- Income from rent could help cover mortgage payments

- You may pay less Council Tax for a property you own or rent that's not your main home

- You still own the property if your circumstances change

- Can provide a steady income stream

Cons

- Stamp duty surcharge of 3% when buying a second property

- You'll have to get a Buy to Let mortgage which often needs a 25% deposit

- Ongoing maintenance costs – budget at least 1% of the property value per year for repairs

- Being a landlord can be time consuming

Things you need to consider when selling

The market

If the value of your home has reduced since you purchased it, you may have to pay off the difference to a mortgage lender. If it seems like the market may be bouncing back, it might not be the right time to sell. However, if you think the market will continue declining in your area – maybe it’s becoming rundown or crime is on the rise – then selling before the value lowers any further might be your best bet.

It’ll also depend on whether there’s a buyers or a sellers’ market when you’re looking to sell. If there’s a frenzy of people looking to purchase property, you may be able to get a premium even if the property isn’t in top shape. Take some time to read about and understand the current market trends. Try speaking with an estate agent if you’re still unsure after some personal research.

Your short-term needs

Selling a property can take a long time and be a disappointment filled process. If your prospective buyers already own a property, there’s often a buying chain that can fall apart at the last moment, putting you back to square one on the day you thought you’d be closing the deal. This isn’t always the case – sometimes things go smoothly on the first try – but if you need to move quickly, then it’s important to know that selling can be a drawn out process.

However, if you’ve been in the property for a long time, the house has grown in value and you have paid off a large portion of your mortgage, then selling could help you obtain a large lump sum of money. While rent gives a long-term income option, it comes in small amounts every month, whereas selling is a one-off large payment. If, in the short-term, you need a large amount of cash for an impending purchase, then selling will be a better consideration.

What are the costs involved with each option?

Renting

While renting can create a long-term income supply, there are also outgoing costs associated with becoming a landlord. While not every cost on this list will be applicable to you, it may help identify some of the costs associated with being a landlord:

Even with the best tenants, things can still go wrong and landlord insurance is there to protect you. There are risks associated with a rented property that won’t be covered under a home insurance policy, so it’s important to make sure that you have the right type of insurance. Without the right cover, unexpected events could leave you seriously out of pocket.

If you were on a regular mortgage while living in a property but are now planning to rent it out, you will likely have to switch to a buy-to-let mortgage. These often require higher deposits than a mortgage for a first property, nearing 15% to 25% of the property value. Speak to your mortgage lender about the options they have available.

An agency may work for you if you live far from the property and can't quickly deal with tenant issue or if you're pressed for time. However, be aware that most agencies will charge around 10% to 15% of monthly rent.

In many flat buildings there is a property management or building factor's fee that takes care of communal areas such as hallways and stairs.

Investopedia suggests using the 'square foot rule' to determine how much you should budget for maintenance. This method suggests that homeowners budget $1 per square foot per year.

The first £1,000 of your income from property rental is tax-free. This is your ‘property allowance’ but after that, you may need to submit a self-assessment tax return. Check HMRC's website for further guidance.

If you're renting in Northern Ireland, Wales or Scotland, then you need to register to be a landlord and often there is a fee associated with this. Some parts of England may require landlord registration as well, so check with your local authority.

Selling:

Though selling a property can quickly provide a large influx of cash into your bank account, there’s quite a few costs you’ll have to deal with in the lead up to your sale. Quite a lot of them are percentage-based to it’s hard to give precise figures, but it will easily be in the thousands. This list may not be exhaustive but here’s a few costs of selling that you should prepare for:

This tax is only for second properties and it won't apply to a main residence. However, if you’re selling a second property that has gained in value since you acquired it, you’ll pay tax on that value increase.

Which? suggests that the conveyance fees from a solicitor can run anywhere from £400 to £1500 but that it could be even higher if the sale is complicated.

Done as a percentage, the Home Owners Association says the average fee is 1.42% of the final sale price.

When looking to sell the house, you may decide to do some small touch ups to help the curb appeal or some major fixes to help boost your home report scores.

These are likely included in the estate agent’s fees, but you should double check what costs you’ll be responsible and which the agent will cover when you decide which one to use.

You’ll be required to have an up to date certificate. They can cost anywhere between £60 and £120 depending on the energy assessor.

A tough decision

This won’t be an easy decision, but hopefully our guide has helped you understand the different considerations that go into selling up or renting out a second property.

If you’re still unsure about what to do, take a look at our complete guide to becoming a landlord, which may help answer any lingering questions you have.